Types Of Compensation

Payroll Basics > Types Of Compensation

Employee Compensation

Employee compensation includes not only direct payments made to employees for work performed but also any benefits indirectly paid on behalf of the employee. The employee's compensation includes not only cash paid to employees but basically anything of value.

As a general rule all types of compensation paid directly or indirectly to an employee is subject to withholding and employment taxes. The IRS does allow an employer to provide some benefits that do provide favorable tax treatment to the business as well as to the individual. In other words, the employer can deduct the expense and the employee doesn't have to include the compensation in his/her earnings.

Note: Rules, laws, and regulations pertaining to fringe benefits are constantly changing. Your type of business organization (sole proprietorship, partnership, LLC, or corporation) may affect the tax treatment of some benefits.

I've grouped an employee's total compensation into four categories:

- Regular

- Additional

- Employer Provided Benefits

- Benefits Provided By Law

Regular Compensation

This is what the employer and employee agreed would be the employee's "regular" pay for the services they provide. Common types of regular compensation are:

- Salaries-compensation based on a fixed amount and paid to an employee for management, professional, administrative, or similar services (exempt type of jobs). A salary is usually stated in terms of a weekly, monthly, or yearly amount. Note: Although salaries are normally used to pay for the so called exempt types of jobs, they may also be used as the payment method for skilled or unskilled employees in non management or supervisory jobs , the so called nonexempt types of jobs. With a "true" salaried position the employee is paid the same amount regardless of how many hours the employee actually works during the pay period.

- Wages-compensation based on an hourly or piece work rate for either skilled or unskilled employees.

- Commissions-compensation based on the employee's productivity usually stated as an amount per sale or as a percentage of each sale. Most commissions are related to selling positions.

- Overtime-premium pay for working more hours than "normal" during a pay period. Normally overtime is paid for all hours worked over 40 in a weekly period. The extra hours are paid at time and a half or in some instances double time. Working on holidays would be an instance when double time might be paid. This type of compensation is not normally paid to management type employees. The government has rules and regulations that apply to this type of compensation.

- Shift differentials-incentive used to attract employees to work during hours that employees would normally prefer not to work. An example would be paying an extra 50 cents an hour to employees who work the midnight shift.

- Paid Breaks-employer pays the employee for the time spent on breaks or rest periods.

Note: Although I differentiated between the terms salary and wages, they are often used interchangeably when discussing pay. In addition, when someone asks the question "what do you make ?" , the answer given normally only includes their regular compensation. As you will see later, fringe benefits can also be a substantial part of an employee's total earnings.

Additional Compensation

Compensation that may or may not be paid to employees based on goals, rules, and regulations determined by the employer or as a customary practice of the industry.

- Tips-extra earnings voluntarily contributed by customers.

- Bonuses and Profit Sharing-extra compensation usually based on meeting or surpassing some company set goals. Normally, but not necessarily, reserved for management type employees. The employer determines the goals, rules and policies that govern the payment of the bonuses.

Note: Bonuses and Profit Share payments are not mandatory payments. The payment of bonuses and profit sharing payments depends on the rules and policies governing the bonus or profit sharing plan.

Employer Provided Benefits

Often called fringe benefits or perks.

Often called fringe benefits or perks.

These type of benefits are normally not paid in cash or included in the employees pay check; however, they are a major cost for most employers (businesses). They can easily amount to 25-30% of an employee's regular wages. Fringe Benefits are not required by law and a business is left to determine what if any benefits they will provide for their employees.

Good employees are one of a business's key assets. Hiring and retaining good employees is a constant challenge. Many businesses "fool" themselves by adopting a philosophy of I don't have to offer much because I can always recruit and hire another body to replace the one that quit. Granted for some low skill jobs they might be right. On the other hand, if this philosophy is used for jobs that require some skill or training provided by your company, you may need to change your philosophy. Turnover is a hidden cost and can "eat your lunch". Work interruptions and slow downs due to untrained or not enough employees can have a drastic effect on a business. Due to the competition from other businesses also wanting to hire and maintain good employees, a business would be wise to investigate and at least offer benefits similar to other businesses in their industry or profession.

What are some of these Other Benefits ?

Some Common Provided Benefits

- Vacation is days off provided to employees to relax and get away from work. The employee is normally allowed so many days off with pay during the year usually based on their length of service (how long they've worked for the company). The longer a person works for the company the more vacation time they normally are provided.

Note: Most businesses allow the employee to select the days; however, some types of businesses may require all the employees to take vacation at the same time. - Holidays are days off for special occasions that the employer provides to employees. The days off can be with or without pay. Normally, the employee gets paid for the holiday after working for the business for a stipulated period of time.

- Sick and personal time is time allowed due to sickness or illness, funerals, jury duty, doctor or dentist appointment, military obligations, etc. This benefit can be with or without pay. Normally sick and personal days are also tied to how long the employee has worked for the company. The employer may or may not require the employee to provide documentation.

- Health insurance provides coverage (payments) for the employee and/or his or her family for medical expenses when a person is sick or injured. The employer can cover the full cost or require the employee to also contribute to the cost of providing this benefit. Normally one of the most wanted benefits by employees. The IRS has some special rules regarding this type of benefit.

- Group Term Life Insurance and/or Disability Insurance – provides payments to the employee or surviving family if the employee dies or becomes disabled. The IRS has some special rules related to this type of benefit.

- Retirement provides a plan to help employees accumulate savings for retirement. Plans may or may not require the business (employer) to contribute to the plan. Most retirement plans are required to follow strict rules and regulations pertaining to eligibility, discrimination, and limits on benefits, and amounts contributed.

Note: Although at one time only thought of as a benefit provided by large companies, more and more small businesses are starting to provide these benefits to their employees. In addition, the laws, rules, and regulations have been simplified in order to encourage small businesses to provide some form of retirement benefits.

Some Other Fringes an Employer May Provide

- Dependent Care

- Continuing Education

- Employee Discounts

- Stock Options

- Parking

- Athletic Facilities

- Meals provided for employer convenience

- Cafeteria Plans

A cafeteria plan is a written plan that allows your employees to choose between cash or non-taxable (qualified) benefits. The IRS has guidelines on what benefits may be offered using these plans.

Note: I have not listed all the benefits imaginable a business has an option to provide as perks to their employees or the resulting tax effects. For an in depth discussion of these and the prior benefits I discussed, visit the IRS's website.

Other Benefits Provided By Law To Employees

These benefits are provided by the employer or a combination of employee and employer contributions.

These benefits are provided by the employer or a combination of employee and employer contributions.

- Worker's Compensation Insurance - a benefit that provides payments to employees for injuries suffered on the job. Only the employer is required to contribute premiums for this coverage. State and federal regulations require most businesses to provide this benefit.

- Unemployment Compensation - a benefit that provides payments to laid off or ex-employees during times when they are not employed. The employer is normally required by law to make payments not only to their state but also to the federal government.

Note:Employees may also be eligible for partial unemployment benefits if working less than full-time.

- Social Security (FICA) and Medicare - a certain percentage is deducted from an employee's pay for FICA (Federal Insurance Contribution Act) and Medicare taxes. The employer is required to pay the same amount as the amount deducted from the employee's wages for these two taxes. In other words, the employer pays half and the employee pays half of these employment taxes.

Note:Earnings from self employment from "flow thru" types of business organizations are subject to special IRS rules pertaining to social security and medicare.

Many employees or for that matter employers don't understand exactly what those FICA and Medicare deductions are and what they do and don't provide to covered employees. Basically, social security deductions (FICA) are for providing some employee retirement benefits and the medicare deduction is used to provide future medical benefits.

The money from social security and medicare deductions goes toward providing the following benefits:

- Retirement - Full benefits are payable at what is called full retirement age (FRA) (with reduced benefits available at an earlier age) to anyone with enough Social Security credits.

- Disability - Benefits are payable at any age to people who have enough Social Security credits and who have a severe physical or mental impairment that prevents them from working or who have a condition that is expected to result in death.

- SSI (Supplemental Security Income) is a benefit paid to people who are over 65 and/or disabled and have low incomes and few resources.

- Family Benefits - If an employee is eligible for retirement or disability benefits and dies, other members of their family might qualify and receive benefits.

- Medicare - Medicare is our country's health insurance program for people age 65 or older. Certain people younger than age 65 can qualify for Medicare, too, including those who have disabilities and those who have permanent kidney failure.

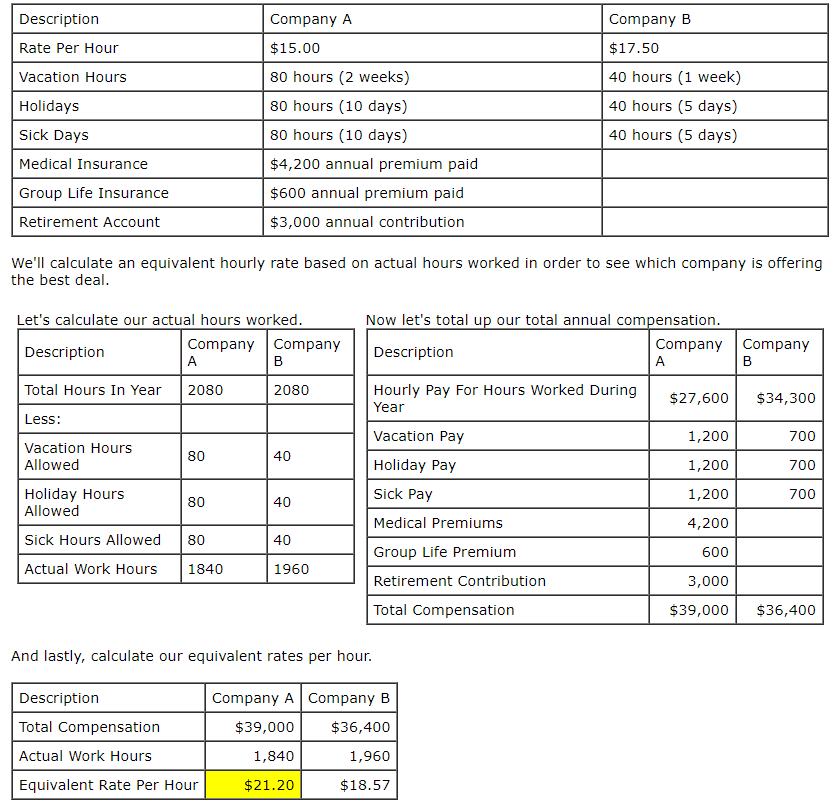

You Be The Judge !

Let's look at a simple example and see which employer you'd rather work for. We'll call them Company A and Company B. We'll use the information and assumptions in the following table to base our decision on.

I know which company I want to work for do you ? I'm going to work for Company A. Fringe Benefits made a big difference.

What's Next ?

Types Of Compensation Video