Final Review

Final Review

Final Review

What We Covered ?

While the emphasis of this tutorial was on Special Journals we also covered quite a bit more !

The Introduction describes the Chart Of Accounts, the Double Entry Bookkeeping System, Accounting Equation, Source Documents, General Ledger, Debits and Credits, and the different types of Special Journals and their Purpose.

Lesson 1 Special Journals, General Ledger Control Accounts, and Subsidiary Ledgers reviews what they are, their purpose, when they are used, and how they are related.

Lesson 2 Sales & Cash Receipts Journals discusses the purpose of these journals, what information is recorded, and provides examples and illustrations of the types of entries that are normally recorded in these journals.

Lesson 3 Purchases & Cash Disbursements (Payments) Journals discusses the purpose of these journals, what information is recorded, and provides examples and illustrations of the types of entries that are normally recorded in these journals.

Lesson 4 Sales & Purchase Return Journals discusses the purpose of these journals, what information is recorded, and provides examples and illustrations of the types of entries that are normally recorded in these journals.

Lesson 5 General Journal discusses the purpose of the General Journal and discusses the types of entries normally recoded in this journal.

Lesson 6 Worksheets and Financial Statements discusses adjusting and closing entries, the Trial Balance Worksheets, and discusses Financial Statements.

Lesson 7 Closing The Books provides examples and illustrations of the how the Worksheets are used, how and why adjusting and closing entries are prepared and posted and the preparation of formal financial statements.

What should we now know ?

Hopefully, you were paying attention "during class" and at least picked up some tid bits of bookkeeping information.

- The General Journal is actually only used to record unusual or infrequent types of transactions. If a transaction doesn't "fit" in any of the other special journals then record it in this journal.

- The purpose of Special Journals, what they are, and how they're used.

- How to determine what Special Journal to use to record the different types of business transactions.

- What Control Accounts and Subsidiary Ledgers are and how they're used.

The general ledger account Accounts Receivable Control includes only total or summary amounts. Since additional detail information about this account is needed, a subsidiary ledger is created that provides this detailed information. Detailed information maintained in the Accounts Receivable Subsidiary Ledger includes:

- Customer Name and Address

- Current Balance Owed

- Amounts Billed-Invoice Numbers and Amounts

- Amounts Paid-Check Numbers/Credit Card/etc.

Also note that every transaction that affects the General Ledger Accounts Receivable Control Account, must be posted both to the Accounts Receivable Control Account in the general ledger and to the individual customer's account in the Accounts Receivable Subsidiary Ledger.

Likewise, since the General Ledger Accounts Payable Control Account only contains summary information an Accounts Payable Subsidiary Ledger is used to record and maintain detail information about suppliers. Detailed information maintained in the Accounts Payable Subsidiary Ledger includes:

- Supplier Name and Address

- Current Balance Owed

- Amounts Billed-Invoice Numbers and Amounts

- Amounts Paid-Check Numbers/Credit Card/etc.

Every transaction that affects the General Ledger Accounts Payable Control Account, must be posted both to the Accounts Payable account in the general ledger and to the individual supplier's account in the Accounts Payable Subsidiary Ledger.

- The flow of information through a bookkeeping system from source documents such as checks and invoices, to the Special Journals, Subsidiary Ledgers, and finally ending up summarized in our General Ledger.

- Closing the books prepares the books for the start of a new period and resets all the income and expense accounts to zero.

- Formal Closing Entries are normally only prepared at the end of a year.

- Adjusting Entries are usually prepared at the end of each accounting period not just at year end.

- The purpose of and how the Income Summary Account is used during our Closing Process.

- Understand how to prepare and use Worksheets as an aid for Adjusting & Closing the books.

- How to prepare our formal Income Statement, Capital Statement, and Balance Sheet with the aid of our Worksheets.

- Steps in Adjusting & Closing Our Books.

- Types of Adjusting Entries.

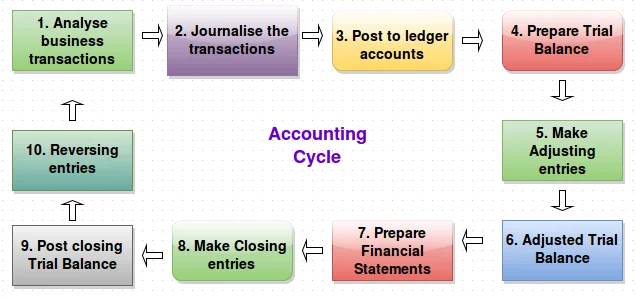

Whether you know it or not, we actually covered the complete Accounting Cycle in this tutorial.

What's the Accounting Cycle ? An accounting cycle is the sequence of repetitive bookkeeping tasks and procedures that are performed each period. Once you get in the groove as a bookkeeper, you basically perform the same tasks each month (period). Basically, all businesses purchase goods and services from suppliers, write checks to suppliers and employees, sell and bill products and/or services to customers, and receive payments from customers and others. Our job as bookkeepers is simply to properly record and summarize these common types of transactions in the proper Journals, Ledgers, Sub Ledgers, and Worksheets.

Steps in the Accounting Cycle

- Identify and analyze transactions that need to be recorded

- Journalize (record) the transactions in the proper journal

- Post from the journals to the General Ledger and Subsidiary Ledgers

- Prepare a Worksheet/Schedule of each Subsidiary Ledger and verify that the total balance of the Subsidiary ledger agrees with the balance of the General Ledger Control Account.

- Prepare A Trial Balance/Adjusting Entry Worksheet

Enter Trial Balance Information from General Ledger

Review accounts and other information to determine if any Adjusting Entries are necessary

Perform any necessary Counts of Inventories

Enter any needed Adjusting Entries in our Worksheet and calculate our Adjusted Balances

- Prepare Worksheet For Closing Entries

Enter Closing Entries to transfer the balances of the Revenue and Expense Accounts to Income Summary Account

Enter Closing Entry to transfer the balance of Income Summary Account to the Owner's Capital Account

Enter Closing Entry to transfer the balance of the Owner's Drawing Account to the Owner's Capital Account - Prepare Income Statement, Balance Sheet and Capital Statement from our Worksheet

- Record our Adjusting Entries in our formal General Journal

- Record our Closing Entries in our formal General Journal

- Post our formal entries from our General Journal to our General Ledger

- Prepare a Post Closing Trial Balance Worksheet

Accounting Cycle Diagram

Food For Thought

Things to think about.

Hybrid Journals

Basic Journals are provided as guides. Remember it's your business and you can design and customize your bookkeeping records any way you want to speed up the recording of your transactions and summarize your business financial activity . Even the IRS, with a few exceptions, allows you to maintain your "books" any way you want as long as they accurately reflect your income.

Normally, you have a separate Cash Receipts and a separate Sales Journal. You could combine them into one.

Hybrid: Cash Receipts-Sales Journal

Record Cash Sales and Charge Sales in the same Special Journal. All sales cash and charge in one place and all your cash receipts in one place.

| Combined Cash Receipts & Sales Journal | Page 1 | |||||||||||

| Entry No | Cash-Debit | Ck No. | Date | Description | Post Ref. | A/R- Debit | A/R- Credit | Sales-Credit | Other | Post Ref | Debit | Credit |

Normally, you have a separate Cash Payments and a separate Purchases Journal. You could combine them into one.

Hybrid: Cash Disbursements-Purchases Journal

Record Cash Purchases and Charge Purchases in the same Special Journal. All purchases cash and charge in one place and all your cash payments in one place.

| Combined Cash Disbursements & Purchases Journal | Page 1 | |||||||||||

| Entry No | Cash-Credit | Ck No. | Date | Description | Post Ref. | A/P- Debit | A/P- Credit | Purchases-Debit | Other | Post Ref | Debit | Credit |

Accounting & Bookkeeping Software

Although many small businesses still use a manual accounting system, due to the reasonable cost (some free) and the benefits of accounting and bookkeeping software, it's difficult to understand why they don't go to a computerized accounting system. A major advantadge is that you can prepare current financial statements and reports anytime instead of having to wait for all the records to be posted and updated using a manual system.

If you completed my Introductory and this tutorial and I did my job, you should be well on your way to becoming an adequate bookkeeper. Sorry I didn't say great, but along with knowledge you also need some experience in order to become great. The more practice or the more you do something the easier it gets. Pretty soon you get to the point where you don't even have to think about it.

By now you should realize that all bookkeeping actually involves is learning some terminology, a few rules and concepts, what records to maintain such as Special Journals and a General Ledger, and applying a little logic and some common sense.

Congratulations

Having completed this tutorial, you shouldn't need as much outside assistance in doing your routine bookkeeping. You know what that means don't you ? Go ahead and cheer while your accountant cries, smaller billings to you for their services. Now you should only need outside help with some of the more complicated tasks.

Cartoons in this tutorial provided by Ron Leishman. If you enjoyed them, get some of your own

What's Next ?

Review Videos