Returns and Allowances

Returns and Allowances

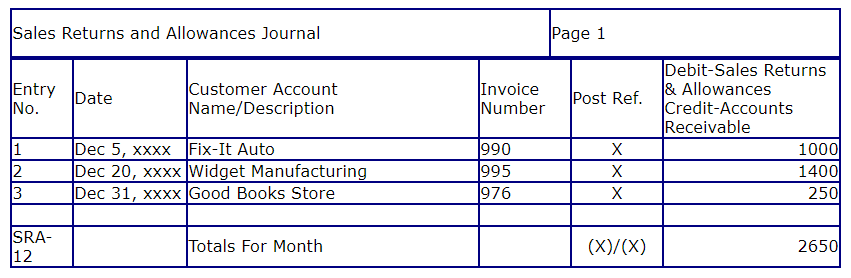

Sales Returns and Allowances Journal

Definition: The Sales Return & Allowances Journal is a special journal that is used to record the returns and allowances of merchandise sold on account.

The entries made in this journal are a credit to the Accounts Receivable Control Account (also a credit to the customer's Accounts Receivable Subsidiary Ledger Account) and a debit to the Sales Returns and Allowances Account.

The source document prepared to document sales returns and allowance can be a "credit" invoice or what is called a credit memo. Why the term credit ? Because we our crediting (reducing) the balance that our customer owes us.

The Sales Return & Allowances Journal has these basic features:

- Header with the Name of the Journal and Page

- Entry Number used as a reference to a specific transaction on the journal's page

- Date Column to record the date of the transaction

- Description Column to record the Customer's name or account and any other explanation or additional information about the transaction

- Reference Column to record our sales invoice numbers

- Posting Reference to provide information when a Subsidiary Ledger also needs to be updated. This tells us whether the Subsidiary Accounts Receivable Ledger has also been posted (updated).

- A Column to debit the Sales Return & Allowances Account and also credit the Accounts Receivable Control Account.

Our illustrated Sales Return & Allowances Journal has a Column for debiting the Sales Returns & Allowances Account and crediting the Accounts Receivable Control Account.

Sample Sales Returns & Allowances Journal

The X's in the Posting Reference Column tell you that the amounts have been posted to the General Ledger and Subsidiary Ledger.

Entry Number SRA-12 is the reference to the Sales Returns and Allowances Journal to use as the reference in the General Ledger Accounts.

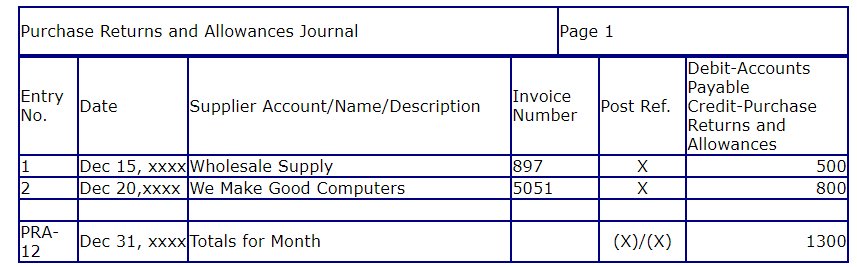

Purchase Returns and Allowances Journal

Definition: The Purchase Returns & Allowances Journal is a special journal that is used to record the returns and allowances of merchandise purchased on account.

The entries made in this journal are a debit to the Accounts Payable Control Account (also a debit to the supplier's Accounts Payable Subsidiary Ledger Account) and a credit to the Purchases Returns and Allowances Account.

The source document prepared by your supplier and sent to you to document your returns and allowance can be a "debit" invoice from your supplier or what is called a debit memo. Why the term debit ? Because we our debiting (reducing) the balance that we owe to our supplier.

The Purchase Returns & Allowances Journal has these basic features:

- Header with the Name of the Journal and Page

- Entry Number used as a reference to a specific transaction on the journal's page

- Date Column to record the date of the transaction

- Description Column to record the Supplier's name or account and any other explanation or additional information about the transaction

- Reference Column to record our invoice numbers

- Posting Reference to provide information when a Subsidiary Ledger also needs to be updated. This tells us whether the Subsidiary Accounts Payable Ledger has also been posted (updated).

- A Column to debit Accounts Payable Control Account and also credit the Purchase Returns & Allowances Account.

Our illustrated Purchase Returns & Allowances Journal has a Column for debiting the Accounts Payable Control Account and crediting the Purchases Returns & Allowances Account.

Sample Purchase Returns & Allowances Journal

The X's in the Posting Reference Column tell you that the amounts have been posted to the General Ledger and Subsidiary Ledger.

Entry Number PRA-12 is the reference to the Purchases Return Journal to use as the reference in the General Ledger Accounts.

What's Next ?

Sales & Purchase Returns Journals Video